Why Americans feel miserable about the economy

Where sentiment and capability intersect -- and where they don't

There is a number created more than half a century ago that captures something Americans understand instinctively: when prices are high, and jobs are hard to find, life gets more difficult.

It is called the Misery Index, and this week we look at what it measures, where it came from, and why it still matters. We take a look at a challenging time for the Federal Reserve, a question from the reader mailbag, a business history story about the late Ted Turner and the launch of CNN, and a closing thought from the great American humorist Will Rogers.

The Brief: The Misery Index Isn’t as Bad as One Might Think

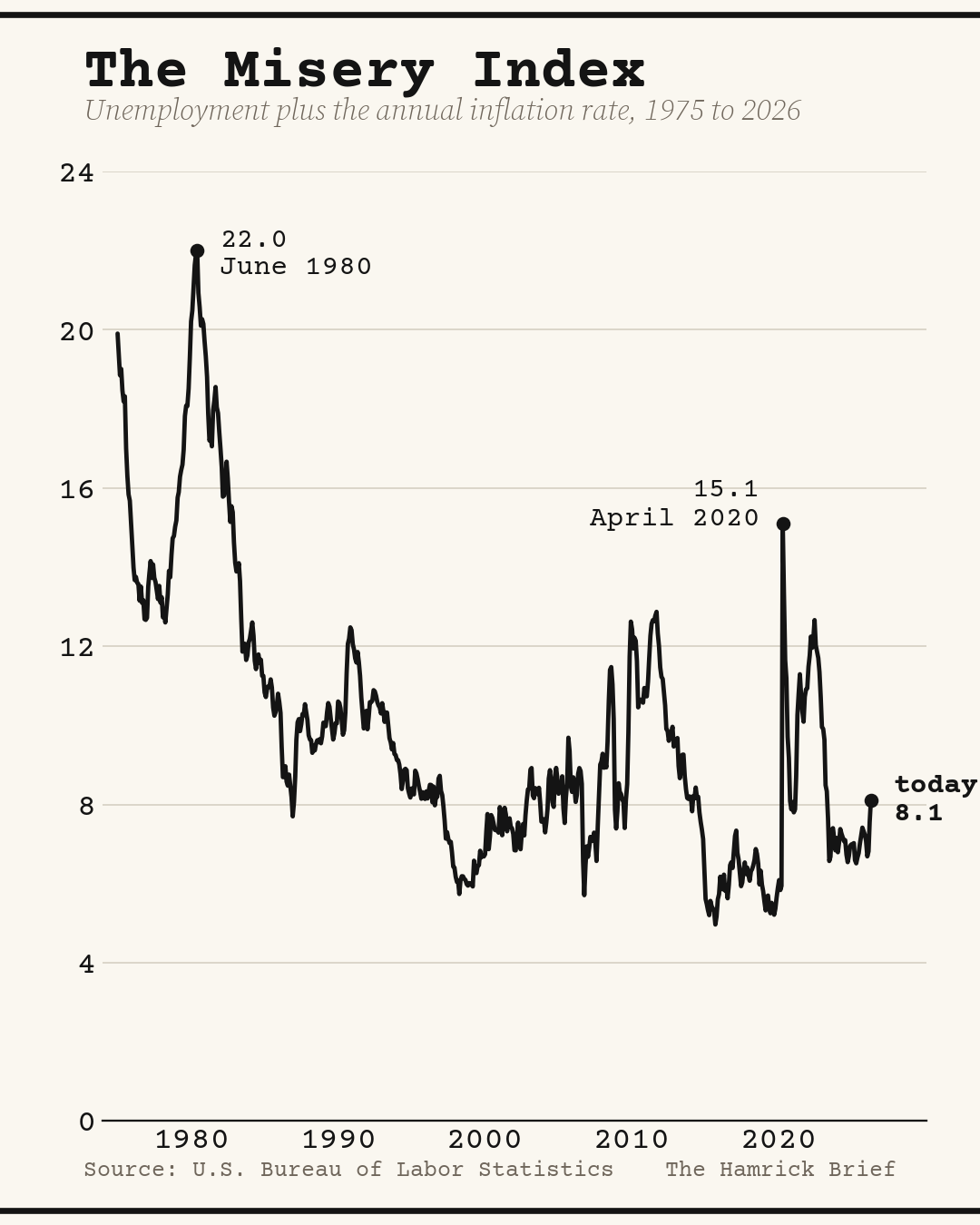

In the 1970s, economist Arthur Okun developed a measure of economic discomfort. He added the unemployment rate and the inflation rate. Simple as that. He called it the Misery Index.

There was nothing especially complicated about it. The logic was straightforward: when people are struggling to find work, and prices are rising faster than paychecks, life becomes more financially stressful.

The index hit its all-time high, near 22, in mid-1980, when inflation was running above 14 percent. Unemployment would climb past 10 percent later, in late 1982, during Paul Volcker’s aggressive campaign to break inflation. Americans who lived through that period hardly needed an economist to tell them the economy felt painful.

So where does the Misery Index stand now? Inflation, measured by the Consumer Price Index, was running at 3.8 percent over the year in April. The unemployment rate stood at 4.3 percent. Put them together, and the Misery Index comes out to roughly 8.1.

That is well below the levels Americans experienced in the early 1980s. But it is also notably higher than the relatively stable years before the pandemic, when inflation was low, and unemployment hovered near historic lows.

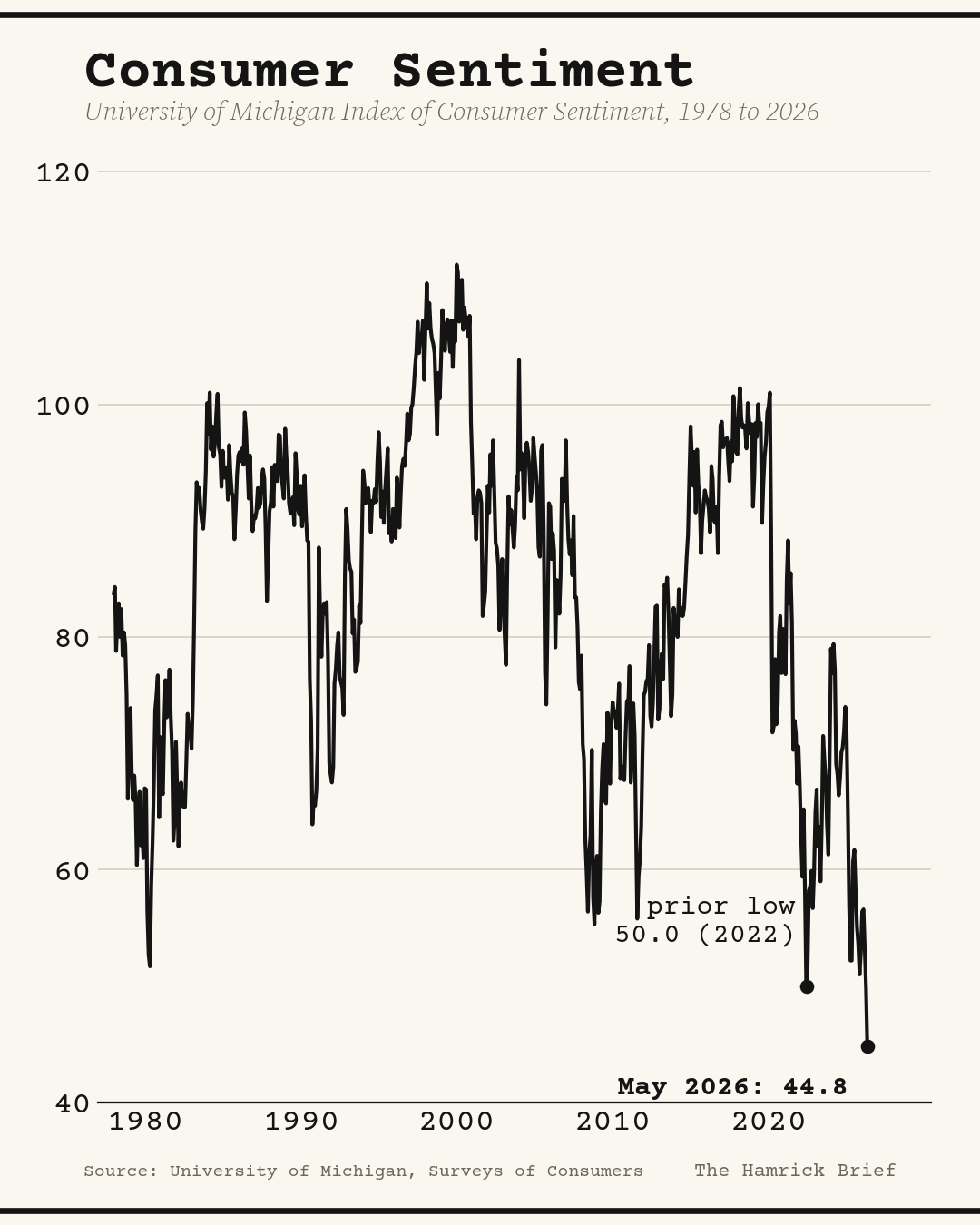

At the same time, the University of Michigan’s consumer sentiment index has fallen to the lowest reading in the survey’s history.

That disconnect helps explain why many Americans still feel uneasy about the economy even when some traditional indicators appear relatively stable.

The Misery Index captures two important pressures: inflation and unemployment. But it does not tell the whole story. It does not measure whether wages are keeping up with costs (not just inflation), whether families feel financially secure, or whether Americans believe their children will have greater opportunity than they did.

Next week, we’ll look at a new attempt to measure Americans’ prosperity.

A New Federal Reserve Chairman Faces Big Challenges

Kevin Warsh has assumed the job of Federal Reserve chairmanship that Jerome Powell held for eight years, inheriting an economy that remains volatile and complex.

Inflation has not fully returned to the Fed’s 2 percent target. The conflict with Iran has led to higher prices for energy and risks passing through to other goods, including food. The labor market is cooling gradually, but has not cracked. Political pressure for lower interest rates appears to have been reserved for former Chairman Jerome Powell, now a board member. Political independence, the cause cited by Powell in deciding to remain a Fed board member, is widely regarded as vitally important for the central bank to be successful.

For now, Warsh and the Federal Open Market Committee appear to be poised to hold steady. Markets have also backed away from aggressive rate-cut expectations that were common earlier this year.

What does that mean for households? The high-rate environment is not ending on anyone’s schedule but the data’s.

If you carry variable-rate debt, including credit card balances, adjustable-rate mortgages, or home equity lines of credit, borrowing costs are likely to remain elevated for a while longer.

Bankrate’s latest weekly survey had the average 30-year fixed mortgage rate at 6.56 percent.

The Fed’s dual mandate, stable prices and maximum employment, translated to low inflation and a healthy job market, reflects the same tension Arthur Okun was trying to capture decades ago with the Misery Index.

Watch the May jobs report, due Friday, June 5. Beyond the headline payroll number (the number of new jobs added or lost) and the unemployment rate, recently at 4.3 percent, pay attention to labor force participation, wage growth, and, as part of the Job Openings and Labor Turnover Summary, the quits rate. The latter is an employment confidence signal. When people believe they’ll find a good job, they feel comfortable quitting. When the job market is more challenging, fewer feel confident about quitting. Those are among the indicators the Fed is watching most closely.

Then & Now: June 1, 1980, Ted Turner Launches CNN

Forty-six years ago today, Ted Turner launched CNN from Atlanta with an idea many people in television considered odd: news twenty-four hours a day. I remember being fascinated by it when attending the University of Kansas as a broadcast news student.

Some mocked CNN as the “Chicken Noodle Network.” Established broadcasters dismissed the concept as unnecessary and financially unrealistic. Turner, after all, was not a traditional network executive. He was a bold entrepreneur and yacht racer who had built a media company through instinct, ambition, and risk-taking.

But Turner understood something many missed: the appetite for information does not operate on a schedule. It was an early bet, ultimately validated, against appointment television, a concept that has faded as consumers have “always-on” access to programming and information.

I have some personal memories of Turner from when I spent time with him at The National Press Club, where I was president in 2011 and an officer, board member and committee chair for years before that. He had a usually charming sense of humor. During a previous visit, he told me that I was wearing my necktie too low. He was right. It was good advice, actually, and I didn’t mind at all.

Back to 2011, we spent time in the historic Press Club president’s office, which I had the privilege of occupying before his appearance with the late pioneering Texas oil tycoon and fierce corporate raider T. Boone Pickens. I don’t remember the name of the woman with Turner, whom he introduced as his neighbor. He quipped, “You know what the Bible says, ‘Love thy neighbor’ “

Suffice it to say, among the five of us, including Pickens’ then-wife Madeleine, I was the least wealthy, by far. They discussed energy policy and climate change. You can watch the archived video with the link below via C-SPAN. Pickens was also quite polite and engaging. The Oklahoma-born billionaire noted that he was familiar with my hometown of Coffeyville, Kansas, which I thought was kind.

https://www.c-span.org/program/national-press-club/renewable-and-alternative-energy/250001

What Turner built reshaped television news and, eventually, the broader media business itself. CNN helped create the modern twenty-four-hour news cycle and changed how governments, corporations, and markets respond to breaking events.

The Gulf War helped elevate CNN into a global institution. The O.J. Simpson trial turned nonstop live coverage into a ratings force. By the time Turner sold CNN to Time Warner in 1996, the operation had become one of the most influential media properties in the world.

Turner died recently, prompting many nostalgic tributes for him and for the ingenious idea that gave rise to CNN and round-the-clock television news. CNN has changed its approach to less news coverage and more commentary with panelists. Previously, there was standalone business and sports programming, which was abandoned. I liked it better before. Personally, I’m not interested in hot takes. I believe they generate mistrust at a time when trust in institutions, including the news industry, is low.

Today, many legacy media companies are confronting the same kind of disruption that Turner created, as audiences continue to migrate toward streaming platforms, podcasts, newsletters, and creator-driven media.

You Asked

“Should I pay off debt or invest right now? I feel like I’m spinning my wheels doing both.” -- Amanda G., Dallas, TX.

This is one of the most common questions in personal finance, and the answer largely depends on the interest rate on the debt.

High-interest debt, especially credit card balances carrying rates around 20 percent or more, should usually be paid down before investing beyond an employer retirement match. There are very few investments that can reliably produce returns anywhere near that level.

Low-interest debt is a different calculation. A mortgage below 5 percent or a federal student loan near 4 percent may allow more room to prioritize long-term investing, particularly inside tax-advantaged retirement accounts.

Historically, diversified stock market portfolios have generated long-run annual returns above those borrowing costs, although past performance never guarantees future results.

Debt in the middle range, roughly 6 to 8 percent, becomes more personal. Some people value the psychological relief of becoming debt-free. Others prefer maintaining a consistent investing habit while gradually reducing debt. Reasonable people can arrive at different answers.

One principle that almost always holds up for workers: capture the full employer match in your 401(k) if one is available. You reduce income tax liability and fund retirement. It is difficult to find another guaranteed return so attractive.

Have a question? Write to me at hamrickusa@gmail.com. I read every message and include reader questions in future editions of The Hamrick Brief.

Last Word

“Even experts don’t know what the weather will do. Even millionaires don’t know what Wall Street will do.” -- Will Rogers, September 6, 1933

Rogers was from Claremore, Oklahoma, not far from Coffeyville, Kansas, where I grew up. The National Press Club -- where I served as president -- is said to have called him “Ambassador at Large of the United States,” which tells you something about how seriously Washington took a man who made his living poking fun at it.

As a young person, I saw James Whitmore perform his one-man show as Rogers. What struck me then, and stays with me now, is how Rogers lampooned politicians of every stripe without malice -- and how that even-handedness is what made people listen.

Next week, we will introduce a new measure of financial well-being, which I’m excited to share.

UMichigan data across ages is pretty uniformly poor, but the Conference Board data shows a widening gap between young and old respondents. It is surprising to see younger respondents being the most optimistic given the doom and gloom hiring environment and inflation.